Raising money is not just about a pitch deck. Understand customer fit, moats, timing, market size, and founder-market fit before your next round.

Founders often measure fundraising success by one number: how much capital was raised. Media headlines are often also framed to focus on that: “Startup X raises €10M,” “Founder Y closes seed round.”

However, a successful round cannot be measured by the size of the check alone. is defined by what that capital eventually enables. Does it help build a stronger company? Does it accelerate growth? Does it create value large enough to justify the investment?

Many founders focus heavily on the mechanics of the pitch itself: perfecting slides, refining design, or memorizing key talking points. While presentation is important, we look beyond the surface. We are searching for signals that indicate whether a founder understands the market deeply, whether the opportunity is large enough, and whether the company can defend itself against future competition.

Beneath all the conversations we have, we often find ourselves returning to a few questions that we decided to discuss in more depth in this blog article.

Fundraising Misconceptions: What Do Investors Care About?

Many founders believe that a great idea is what gets investors interested. It sounds reasonable, but that is usually not how investment decisions are made.

Investors are exposed to an enormous number of ideas every year. Most concepts have already been seen in some form, and many of them can sound exciting on the surface. The difference is rarely the idea itself.

What investors want to understand is whether this particular company can turn an opportunity into something much larger. They want to know who the customer is, why the problem matters now, why this team is positioned to solve it, how large the market can become, and why competitors will not simply replicate the approach.

Some of the most common misconceptions include:

- “If the market is large, investors will invest.” – A large market matters, but market size alone is not enough. Investors also want to know whether the company can realistically capture a meaningful share of it.

- “The pitch deck is what closes the round.” – A deck opens conversations. It does not close them. The real process happens in discussions around execution, assumptions, and future growth.

- “Innovation alone creates defensibility.” – Having a unique product is valuable, but investors also ask whether competitors can replicate it quickly.

Once the discussion moves beyond broad assumptions and high-level narratives, the conversation becomes much more practical. Investors start narrowing in on the details that determine whether an opportunity is real.

And one of the first areas where many startup pitches fail to fulfill their mission is customer definition. Founders often describe industries, markets, or categories of companies. Investors are trying to understand something much more specific: who exactly has the problem?

Before investors believe in a solution, they need confidence that they understand the person who needs it.

That brings us to one of the first questions that we often found ourselves asking:

1. Can You Describe Your Customer Without Describing The Market?

Founders often describe industries, broad segments, or company types because it feels like they are defining the opportunity:

“Enterprises struggle with compliance complexity.”

At first glance, that sounds reasonable. But it doesn’t actually tell investors who experiences the problem, where the pain exists, or why it matters enough to create urgency.

“Enterprises” are not customers. They do not feel frustration, lose time, or make buying decisions. People do. So, let’s try to refine that into a stronger version: “A Head of Compliance at a 200-person fintech company loses 14 hours every week to manual reporting processes.”

- The first example describes a market.

- The second describes a person, a context, and a measurable problem.

The more specific the answer becomes, the easier it is to understand whether a real opportunity exists. Markets create categories. Customers create companies.

This is exactly what investors want to understand:

- Who specifically experiences the pain?

- What triggers the problem?

- How often does it happen?

- What is the cost of ignoring it?

- Who ultimately makes the buying decision?

2. Can You State Your Moat Without Using “Team,” “Speed,” or “First-Mover Advantage”?

Another common weakness in startup pitches appears when founders start talking about competitive advantage. Almost every founder believes they have one.

Team, speed, and first-mover advantage are the weakest moat claims that a founder can use. We heard them countless times before, and on their own, they rarely create meaningful defensibility.

None of these advantages is difficult to replicate, because competitors can:

- Hire talented people

- Raise capital

- Move faster than you

- Release similar products

- Copy features and positioning

Being first can help create an early lead, but history shows that being first rarely guarantees winning the market. In many cases, larger or better-funded companies eventually enter and scale faster.

We look for advantages that become stronger over time and harder to reproduce. That can include:

- Proprietary data that improves the product over time

- Unique distribution channels that competitors cannot easily access

- Network effects, where the product becomes more valuable as adoption grows

- Exclusive partnerships or access

- Regulatory advantages or certifications

- Deep workflow integration that makes switching difficult

This question matters even more today because technology is becoming easier to replicate, and AI is influencing how products are built. We worry less about whether a product can be created and more about whether it can remain differentiated over time.

3. Is Your “Why Now” a Trigger or a Trend?

One of the most overlooked parts of a startup pitch is explaining why the company makes sense now rather than three years ago, or three years from now.

We often hear it described in broad terms: “AI is changing everything” or “Automation is becoming essential.”

The problem with these descriptions is that they apply almost everywhere. These trends describe direction, but they do not connect with real timing. Additionally, if we hear this from every company out there, it doesn’t sound like differentiation anymore; it’s just noise that we want to ignore.

What we are looking to find beyond this is the trigger. A trigger points to a specific event that changed market conditions. Can you identify the month when something changed?

- January: this regulation changed

- March: the costs of infrastructure for this dropped

- June: this particular technology became usable at scale

- September: this segment of customer behavior changed

If you cannot identify the month something changed, you are probably describing a trend rather than a timing opportunity.

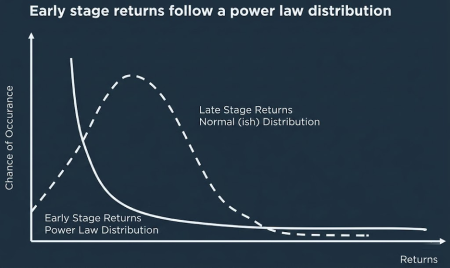

4. Have you done the fund return maths on your TAM?

One of the most common misunderstandings around fundraising is assuming that market size alone drives investor interest. Founders often present TAM figures as evidence that the opportunity is large:

“This is a £20 billion market. We are targeting a massive global opportunity.”

The problem is that large markets alone do not explain investment returns. They sound impressive, but are doing a different math on the paper.

Venture investing operates on a power-law model. A fund writing £5M checks is not looking for outcomes that become £50M companies. It needs a small number of investments to produce disproportionately large outcomes.

That means looking backward:

- How much ownership could we realistically maintain?

- What could this company be worth at exit?

- What multiple does that create on invested capital?

- Is that return meaningful at the fund level?

And probably one of the difficult questions to answer is: Can your company realistically become a £500M+ company?

Because if the numbers do not work at the fund level, the opportunity may still become a great company; it just may not become a venture-scale one.

5. What Makes Your Team Special For This Specific Problem?

Many founders assume that a strong team slide automatically strengthens a pitch.

They list previous roles, recognizable employers, years of experience, and achievements that demonstrate competence. These details help establish credibility, but they often miss the question investors are actually trying to answer.

Experience doesn’t create defensibility. Investors know that strong teams can be assembled. Attractive markets eventually draw talented people, experienced operators, and larger companies with more resources. Competitors can hire talented people. Capital can attract strong operators. Well-funded companies can build teams quickly.

Instead, investors are trying to understand founder-market fit more deeply.

- Why is this team unusually equipped to solve this problem?

- What insight exists because of their background that others may not have?

- What access, understanding, or perspective creates an advantage beyond credentials?

Sometimes the answer is deep customer relationships. Sometimes it is industry knowledge developed over years of direct exposure. Sometimes it is understanding a problem from the inside in a way that outsiders never could.

That is up to you to find your unique angle. 😀

Final Thoughts Before Your Next Round

Before entering investor meetings, it is worth treating your own pitch the way an investor would. Take away the excitement, the narrative, and the presentation layer, and ask yourself these uncomfortable questions above.

We are not expecting perfect answers. Early-stage companies are built around uncertainty, and experienced investors understand that. We just want to see clarity of thinking.

- Can you explain not only what you believe, but why you believe it?

- Can you identify the assumptions that your business depends on?

- Can you tell the difference between what you know, what you think, and what you still need to learn?

A round should not simply validate that you can raise capital. It should validate that you understand the company you are trying to build, the market you are entering, and the reasons why this opportunity deserves to exist.